- Cotribute

- Posts

- Why Frictionless Business Account Opening Is the Key to Winning Today’s SMBs

Why Frictionless Business Account Opening Is the Key to Winning Today’s SMBs

Philip Paul

April 22, 2025

Business banking has reached a tipping point. Small-to-medium businesses (SMBs) no longer tolerate clunky, branch-bound onboarding processes. Instead, they expect digital-first experiences that are simple, secure, and fast. Nearly 80% of SMBs now prioritize streamlined digital services when choosing a financial partner.

For bank and credit union CEOs, that means one thing: modernizing the business account opening experience is no longer a nice-to-have—it’s a strategic imperative. In this article, we break down what business customers want, how automation helps financial institutions keep up, and the steps to modernize onboarding to drive growth, reduce fraud, and strengthen customer relationships.

1. SMB Expectations Are Shaped by Fintechs

Today’s business owners live online. They manage their companies with mobile apps and cloud platforms, and they expect the same from their bank. They want to open business accounts remotely, without paperwork or branch visits. And they expect this process to be fast, intuitive, and error-free.

Consumer fintechs and neobanks have set a high bar. Many allow users to open accounts in minutes—a standard that business owners now expect across the board. According to Cornerstone Advisors, user experience is the new competitive edge. As a result, SMBs increasingly shop for banks that offer modern digital features, even if that means moving away from their current institution.

Surveys show that 41% of SMBs are likely to switch banks, and the number one reason is poor digital experience. Meanwhile, two-thirds are actively exploring new banking relationships that offer better technology and services. This presents a huge opportunity for forward-looking financial institutions. Those who invest in seamless digital onboarding will gain a decisive edge in acquiring and retaining high-value business clients.

2. Account Opening as a Growth Lever

Digital business onboarding is more than operational efficiency—it’s a revenue driver. By removing friction from the onboarding process, banks and credit unions can:

Boost deposits: A streamlined experience encourages more businesses to open accounts, fund them quickly, and consolidate their banking needs with one provider.

Grow lending pipelines: Business deposit accounts often serve as the first step in a broader lending relationship. Simplified onboarding increases the likelihood of future credit and loan products.

Expand reach: With remote onboarding, geography is no longer a barrier. Institutions can attract customers beyond their branch network, unlocking new markets without adding physical locations.

A high-quality onboarding experience leads to stronger conversion, higher balances, and longer-lasting relationships. In fact, Cornerstone research shows that banks with mature digital onboarding capabilities grow deposits and loans faster than those that rely on legacy workflows.

3. Automating KYC/KYB and Reducing Fraud

Manual compliance checks are slow, error-prone, and resource-intensive. Automation changes the game.

With real-time identity verification, applicants can scan a government-issued ID and validate their identity in seconds. Facial recognition and liveness checks ensure authenticity, reducing the risk of impersonation.

Meanwhile, KYB automation verifies business entities via public databases and pulls relevant compliance data instantly.

This kind of automation enables straight-through processing—in many cases, applications can be approved or declined without any human intervention. That not only accelerates onboarding but reduces fraud exposure and regulatory risk. Instead of manually reviewing every application, compliance teams can focus on exceptions and high-risk cases.

Automated watchlist screening (OFAC, PEP, etc.) and fraud scoring engines add another layer of security, consistently applying advanced fraud detection across every application. For CEOs, the takeaway is clear: automation improves both speed and safety.

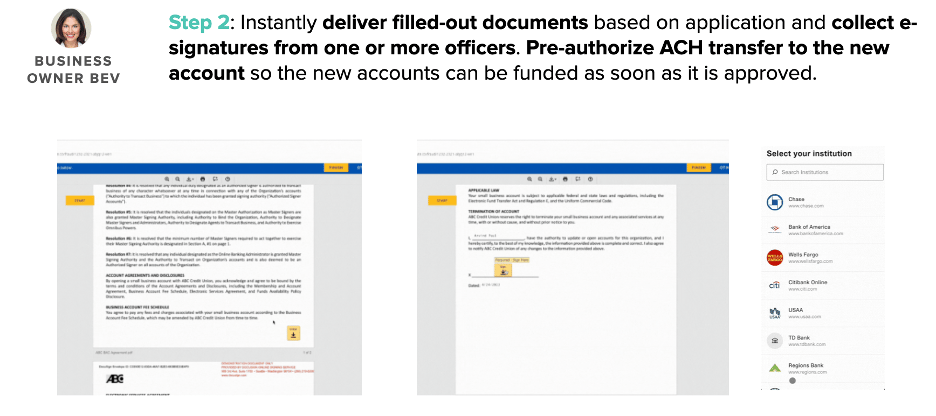

4. Streamlining Document Collection and Due Diligence

Traditionally, business account opening involves fragmented document collection: emails, faxes, phone calls, and branch visits. It’s inefficient and frustrating for customers and staff alike.

Modern platforms centralize this process. Business owners can upload formation documents, licenses, and IDs through a secure online portal. Built-in checklists ensure they provide the right documents based on entity type. Optical character recognition (OCR) and AI can even validate document accuracy and extract relevant data automatically.

E-signatures make paperwork seamless. All required parties—owners, signers, guarantors—can review and sign from anywhere. The result is a fully digital file that’s complete, compliant, and ready to go.

With reminders and progress tracking built in, applications don’t stall out due to missing info. The impact on onboarding times is dramatic: hours or days are reduced to minutes, and staff bandwidth is freed up for more valuable activities.

5. Core and System Integrations Are Essential

Automating the front end of onboarding isn’t enough—the real value comes when that data flows directly into the core banking system.

With real-time integration, approved applications trigger automatic account creation, generate account numbers, and initiate service setups like online banking or debit card issuance. There’s no need for manual re-entry, reducing errors and increasing speed.

Beyond core systems, integration with CRM, loan origination systems, and document archives ensures a unified, end-to-end experience. For example, identity-verified data can automatically pre-fill a loan application. CRM integration ensures relationship managers have full context for follow-up or cross-sell conversations.

This kind of automation eliminates data silos, enhances operational accuracy, and supports real-time analytics and reporting—essential for compliance, marketing, and strategy.

6. Composable, No-Code Platforms for Agility

Digital onboarding platforms should adapt to your institution’s needs—not the other way around. A composable architecture allows banks and credit unions to mix and match the components they need, from identity checks to KYB tools to e-signatures.

With no-code configuration, teams can customize workflows, update forms, and implement rule changes without writing software. This enables rapid response to regulatory updates or new product launches. If a new account type is introduced, the workflow can be spun up in days instead of months.

Composable systems also support better integration with fintech partners, enabling embedded banking services or specialized tools. And because they overlay existing infrastructure, they eliminate the need for costly rip-and-replace implementations.

In short, a flexible platform ensures your institution can keep pace with change while delivering the customized experiences your business clients expect.

7. Prioritize 18 Key Features in Your Digital Onboarding Solution

When evaluating or building a digital business account opening solution, bank and credit union leaders should ensure certain core capabilities are in place. Below are 18 key automation and experience features that modern institutions should prioritize to deliver a world-class onboarding journey for business customers:

End-to-End Digital Application – A fully online account opening process that business owners can complete remotely, from initial application to final signature, without paper or branch visits.

Anytime, Anywhere Access – Mobile-friendly and responsive design so that applicants can initiate and finish onboarding on any device (phone, tablet, or desktop) at their convenience.

Multi-Owner/Signer Support – Ability to collect information and e-signatures from multiple business owners or authorized signers within a single application workflow (critical for partnerships, LLCs, corporations, etc.).

Personalized Workflows – Configurable application paths that adjust based on the customer type or risk profile (e.g. different steps for a brand-new client vs. an existing customer or streamlined flow for low-risk sole proprietors).

Automated Identity Verification (KYC) – Integration of real-time ID verification (driver’s license scan, selfie match, biometric checks) to confirm individual identities instantly and detect fraud.

Business Entity Verification (KYB) – Automated lookup of business details through databases (EIN validation, Secretary of State records, business credit bureaus) to verify the business’s legitimacy and status.

Beneficial Ownership Capture – Built-in collection of required beneficial owner information and control person details, with threshold tracking (e.g. identifying all owners with 25%+ ownership) to satisfy FinCEN’s Customer Due Diligence rules.

Watchlist and Sanctions Screening – Automatic cross-checking of all parties against OFAC sanctions lists, politically exposed persons (PEP) lists, and other watchlists as part of due diligence, with alerts for any potential matches.

Risk Scoring and Flagging – An internal risk engine that scores applications based on factors like business type, credit history, fraud signals, etc., and flags high-risk cases for manual review while green-lighting low-risk ones for instant approval.

Secure Document Upload Portal – A user-friendly interface for applicants to upload required documents (e.g. formation documents, IDs, licenses) directly, with encryption and security, replacing email or in-person drop-offs.

E-Signature Integration – Seamless electronic signing of account agreements and forms by all necessary parties during the workflow, creating a legal e-paper trail and eliminating the need for wet signatures.

Core Banking System Integration – Pre-built connectors or APIs to push new account data into the core system in real time, so that approved accounts are created automatically with no re-keying.

LOS/CRM Integration – Hooks to loan origination systems and customer relationship platforms to share data (for cross-sell or simultaneous deposit & loan onboarding) and to avoid duplicate data entry across systems.

Real-Time Funding Options – Options for the customer to initially fund the new account digitally (via ACH transfer from an existing account, credit/debit card, etc.) as part of the onboarding, enabling faster activation.

Workflow Management Dashboard – A consolidated back-end portal for staff to view all pending applications, verify information, handle exceptions, and track progress, ensuring transparency and oversight of the onboarding pipeline.

Audit Trail & Reporting – Automatic logging of all application actions, decisions, and data changes, with the ability to generate reports for compliance audits and internal tracking of onboarding performance (e.g. cycle times, approval rates).

Modular/Composable Architecture – A system design where features are modular and interoperable, making it easier to integrate new services or adapt the process without rebuilding from scratch (e.g. swap out a KYC provider module as needed).

No-Code Configuration – Administrative tools that allow your team to adjust forms, fields, decision rules, and workflow logic through an intuitive interface, rather than requiring custom coding – enabling faster updates and institution-specific customization.

Conclusion: Digital Onboarding of Business Accounts Is a Strategic Advantage

Modernizing business account opening is no longer optional. In a market where SMBs expect fast, digital-first banking, financial institutions that fail to deliver risk losing valuable relationships to more agile competitors.

By digitizing and automating onboarding, banks and credit unions unlock real business value:

Faster onboarding translates to more accounts and earlier deposits.

Automation reduces fraud and compliance risk while freeing up staff.

Integrated systems create a seamless experience from application to activation.

Composable platforms allow you to innovate and scale without disruption.

The right onboarding solution should be a growth engine and a competitive differentiator. And the right partner should act as a strategic collaborator—not just a software vendor.

By aligning technology with business strategy, CEOs can turn onboarding into an opportunity for smarter, safer, and more scalable growth.

It’s time to meet your business customers where they are—online, on demand, and ready to grow with you.